Buying a home in Canada is an exciting journey, but there are a lot of steps to walk through before throwing that housewarming party. One of the most crucial steps of the home-buying process is acquiring a mortgage loan. Not only does a mortgage loan help you to be able to purchase a home in the first place, but the mortgage loan process also helps you to understand how much house you can realistically afford.

We have laid out a 7-step guide to the mortgage loan process in Canada. While the process may slightly vary between buying Regina real estate and Toronto real estate, the basics are the same across the board. Follow along to learn more about the mortgage loan process in Canada.

Different Types of Mortgage Lenders

There are a plethora of options available during the mortgage loan process, one of which is the type of lender you get your mortgage loan from. Some bigger lenders like Scotiabank are common but may have harsher loan qualifications, while smaller banks may have a higher interest rate but are more flexible when qualifying for a loan. Here is the breakdown of the different types of mortgage lenders in Canada:

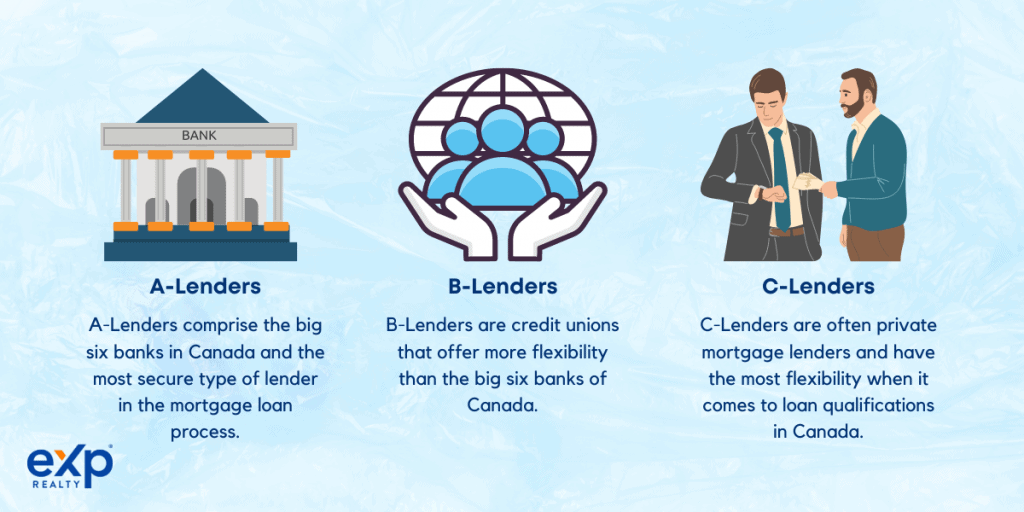

A-Lenders

A-Lenders comprise the big six banks in Canada: the National Bank of Canada, Royal Bank, the Bank of Montreal, Canadian Imperial Bank of Commerce, the Bank of Nova Scotia (Scotiabank), and Toronto Dominion Bank. The most secure type of lender in the mortgage loan process, A-Lenders have moderate interest rates but the strictest qualifications.

To qualify for a loan from an A-Lender, you’ll likely need to verify and prove steady employment and have a credit score of 680 or higher.

B-Lenders

B-Lenders are credit unions that offer more flexibility than the big six banks of Canada. An excellent option for those who don’t qualify for a mortgage loan from A-Lenders, credit unions have more wiggle room than larger lenders to adjust the terms of your mortgage. For this reason, interest rates are typically lower from credit unions.

To qualify for a mortgage loan from a B-Lender in Canada, you’ll most likely need a credit score of 600 or higher.

C-Lenders

C-Lenders are your best option if you don’t qualify for A- or B-Lenders. C-Lenders are often private mortgage lenders and have the most flexibility when it comes to loan qualifications in Canada. Note that C-Lenders often have higher interest rates to make up for “riskier” clients, but you’ll only need a credit score of around 550 to qualify for many mortgage loans from private lenders.

PRO-TIP: A C-Lender is great to use when buying your home, but try using an A- or B-Lender to refinance to take advantage of lower interest rates in the future.

What Do Mortgage Lenders Look For?

In order to qualify for a mortgage loan, lenders tend to look at three main factors. Here’s a little bit about each one and how to best prepare yourself for the mortgage loan process in Canada.

Credit Score

When considering your application in the mortgage loan process, any lender will look at your credit score to see if you are a reliable borrower. A high credit score ensures that you have a history of making payments on time, letting a lender know that you are likely to make all your mortgage payments. The higher your credit score is, the more options you’ll have for getting a mortgage loan.

According to Equifax, the average homebuyer in Canada has a credit score of 753, but yours doesn’t have to be this high to qualify for a loan. In general, if you have a credit score of 600 or lower, you’ll likely have to find a private lender for your mortgage loan. If you have a credit score of 680 or higher, you’ll have the widest array of loan options available to you.

Some methods of increasing your credit score before applying for a mortgage loan include:

- Paying bills on time

- Using less than ⅓ of your credit limit at a time

- Diversifying your credit mix

Income

During the mortgage loan process, lenders will look at both your source of income and how much income you make. Know that, for most lenders, you’ll need to provide proof of income through pay stubs, a letter of employment, and/or bank statements. If you are self-employed, which is a prevailing situation for homebuyers that work from home, you may need to show your tax returns from recent years to prove your income.

When looking at how much income you have, lenders generally want to ensure that no more than 39% of your income is spent on the following:

- Mortgage Principal and Interest

- Property Taxes

- Heating and Utilities

These three factors are commonly referred to as PITH, and it’s relatively easy to check how much of your income is going toward those factors before meeting with a lender. In addition to testing your PITH ratio, lenders may conduct a mortgage stress test to determine whether or not your current income would allow you to continue to pay your mortgage if rates were to increase.

The best way to prepare for the mortgage stress test is to test your current income against your desired interest rate and then increase that rate by 2% and again by 5.25% and see if you’d still be able to pay your mortgage each month. Of course, lenders will do this math for you, but if you want to prepare for those lender conversations ahead of time, we recommend doing some of the math yourself.

Down Payment

The final factor that mortgage lenders look at during the mortgage loan process is how much of a down payment you can and are willing to put down. Typically, the larger your down payment, the lower your mortgage will be. However, the down payment expected from buyers depends on the kind of property you need a mortgage loan for. Here’s the breakdown:

- Primary Residence: 5%-10% minimum down payment

- Secondary Residence: 5%-10% minimum down payment

- Investment Property: 20% minimum down payment

- Commercial Property: 25% minimum down payment

- Raw Land: 30% minimum down payment

Keep in mind that it’s always possible to negotiate with your lender on mortgage and interest rates, but if your down payment is on the lower end of the spectrum, you’ll likely owe more interest and spend a long time paying off the property.

7 Steps to Getting a Mortgage Loan in Canada

![]() Now that we’ve discussed the ins and outs of preparing for the mortgage loan process in Canada, here’s a step-by-step guide that will help you see what the process looks like as a whole.

Now that we’ve discussed the ins and outs of preparing for the mortgage loan process in Canada, here’s a step-by-step guide that will help you see what the process looks like as a whole.

1. Initial Discussion

First, you’ll want to have an initial discussion (or discovery call) with at least three different lenders. Not only do you want to have different rate and interest options, but you want to ensure that you are working with a qualified and reliable lender. This is less of a concern when getting a mortgage loan from an A-Lender and more important when seeking a loan from a private lender.

2. Loan Application + Documentation

After finding a dependable lender to walk you through the mortgage loan process, you’ll need to submit your loan application and provide documentation. Here is where you will put in your general and desired property information and attach any employment or income documents for your lender to test.

3. Pre-Approval

Once you submit all your mortgage support documents for approval, the lender will look through the papers and pull together a list of mortgage loan options that best fit your needs and financial situation. Depending on how quickly you are able to provide all the necessary documentation, this could take anywhere from 24 hours to a week or more.

In this step, your lender will also pre-approve you for your loan. This is a temporary declaration from the lender stating that you are likely to be approved for the mortgage loan of your choosing and allows you the confidence to move forward in your property search.

4. Lender Underwriting

Once you have the desired property, your lender will weigh the property price against your income, credit score, and down payment savings to determine the best loan option for you. In this step, the lender will let you know if you are searching for homes with too high of a price, and they will be able to see if anything has changed in terms of your income. After all this testing, your lender will approve or deny your loan application.

5. Conditional Commitment Processing

Once your application is approved, the mortgage loan process continues with conditional commitment processing. This is where your lender creates a conditional document stating the terms of your loan and any other necessary legal information. Once you receive and sign this document, your lender will send a copy to your lawyer of choice and REALTOR (if applicable) to let them know your funding has been approved.

6. Pre-Closing

Pre-Closing is where your lawyer and mortgage lender work together to prepare and register the mortgage with the Land Titles Office. In the case of a successful purchase, they will also transfer the property title to you. To lock in everything properly, you’ll need to set aside time to meet with your lawyer to sign papers, provide a down payment and closing costs, confirm needed insurance, and tie up any other loose ends.

NOTE: During this phase, it is crucial that nothing changes in terms of your income or credit situation, as your lender could still back out at this point.

7. Closing

During closing, your lender will transfer the mortgage funds to your lawyer’s trust account, and your lawyer then ensures that the money gets where it needs to go. This is where your REALTOR provides you with your keys, and your name is officially registered on the title! The loan is now closed and you are officially a homeowner!

The 7-Step Guide to the Mortgage Loan Process in Canada

We hope this article clarified the different steps of the mortgage loan process in Canada and helped you understand what lenders are looking for when applying for a mortgage loan. To ensure that this is a seamless and successful process, it’s best to have a designated lawyer and a local real estate agent on standby.