When buying a home in Canada, it might seem like you’re walking into a minefield blindfolded. Really though, buying a house doesn’t have to be that nerve-wracking so long as you use an agent, your common sense, and give yourself plenty of time to hunt for homes for sale in Canada and save up money. That being said, there are a few dos and don’ts that might not seem obvious to you if this is your first time buying a home. If that’s the case, we’ve compiled a brief list of the best practices and worst mistakes you can make when buying a home in Canada.

Do’s

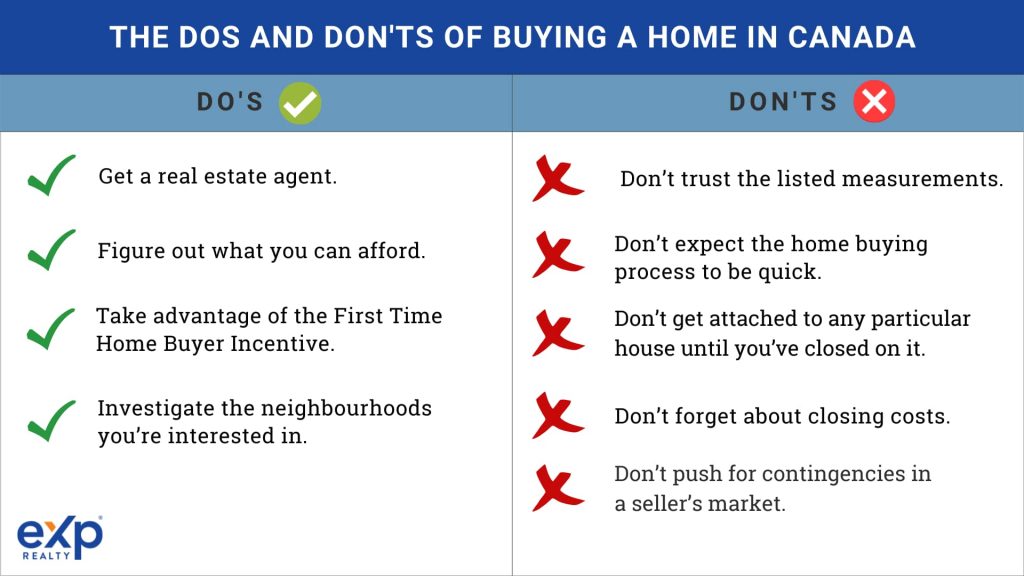

Get a real estate agent

We can’t stress this one enough. Trying to be your own real estate agent in today’s market is like trying to represent yourself in court. It’s a bad idea.

Let’s say you’re moving to Toronto from out of town. Nine times out of ten, your agent will know more about your local market than you, know more about the home buying process than you, and know soon whether you’re getting a good deal on your home. When looking for a real estate agent, be sure to choose someone who has a few years of experience in the profession and knows your desired neighbourhood’s well.

Figure out what you can afford

A lender can help you do this, but generally you need to focus on a few key percentages that will make sure that, after you close on a house, you can actually afford to keep it.

Generally, you don’t want your monthly housing costs to rise above 35% of your monthly income. This includes your mortgage payments, repairs, utilities, etc. Go above that 35%, and you’ll see your savings erode. Add any other debts to those associated with your house and try to keep your gross expenses below 42%. If you’ve considered the house you want to buy and done the math, and you find that you’ll be spending more than you can afford, step away.

Take advantage of the First Time Home Buyer Incentive

If you’re a first-time home buyer in Canada, you may be eligible to profit from this government program that lends 5%-10% of your home’s value to you in order to be used on your down payment. Make sure to get properly informed about the nitty gritty details of the FTHBI program before deciding to apply.

Investigate the neighbourhoods you’re interested in

It’s time to play detective. Though you don’t need to do a 48-hour stakeout to get the low-down on the neighbourhood of your dreams, you should head over there occasionally to get a feel for the place. Drive around and see how the traffic is. Take a walk on a Sunday morning and Saturday night and make sure you feel comfortable both times.

Don’ts

Don’t trust the listed measurements.

If you’ve got the time and the inclination, do your own measurements of the houses you’re interested in or get an inspector to do it for you. If the measurements are off from what the seller listed, it’s probably not a case of them lying but taking the measurements straight from the architectural plans of the house, which don’t always line up with reality. Regardless, taking measurements is a simple and straightforward process that can’t hurt to try.

Don’t expect the home buying process to be quick.

Buying a home in Canada, especially in hot markets, can be a real test of your patience and endurance. You might bid on a dozen homes in two months and not land on a single one. You need to be ready to spend weeks if not months trying to lock down a home. So if you’re planning some delicate time windows where you’ll be moving seamlessly from one house to another, think again.

Don’t get attached to any particular house until you’ve closed on it.

We mean to say: don’t count your chickens till they hatch. For any number of reasons a deal can fall through at any moment in the home buying process, especially in more competitive markets. It’s easy and natural to get personally attached to a home you really, really want, and you should get attached to it, but only once you know beyond a shadow of a doubt that it’s in your hands after closing and funding.

Don’t forget about closing costs

There’s a catch to everything, including buying a home. People don’t realize that there are hidden costs both to buying and selling a home, some of which get passed on to the seller and some which get passed on to the buyer. You, the buyer, need to keep in mind some closing costs: the Land Transfer Tax, title insurance, home insurance, legal fees, mortgage set-up costs, and utility and property tax costs.

Don’t push for contingencies in a seller’s market

Love it or hate it, if you’re in a seller’s market, using contingencies as a buyer makes your bid look very attractive and risky to the seller. You may be looking for a home for sale in Vancouver, but so are about thirty other people. Chances are high, if not certain, that at least half of those bidders have waived their rights to back out of the deal if the property in question has any problems with it, or if they’re unable to secure financing. These rights, or contingencies, are great if you’re in a buyer’s market and have leverage over the seller. But if you’re in a hot enough market, they’ll just hamstring you.