Sometimes when you see a price tag on a home for sale that’s too good to be true, it may be branded as a short sale. With short sales, the price tag is real, but the transaction comes with some stipulations as the seller needs to sell their home before the lender forecloses on it. If you’ve fallen into hard times and are considering listing your home for sale in Toronto or you’ve come across a good deal in the Vancouver real estate market, continue reading to learn what a short sale in real estate is.

What Is A Short Sale In Real Estate?

When you see a short sale property, it means the seller has fallen into financial troubles and is needing to sell their home before the lender forecloses on it. A short sale is a way for the lender and borrower to settle a debt the borrower can’t pay and oftentimes allows a buyer to get a good deal on a home. When a short sale in real estate happens the lender receives all the earnings from the sale of the property.

When you see a short sale property, it means the seller has fallen into financial troubles and is needing to sell their home before the lender forecloses on it. A short sale is a way for the lender and borrower to settle a debt the borrower can’t pay and oftentimes allows a buyer to get a good deal on a home. When a short sale in real estate happens the lender receives all the earnings from the sale of the property.

This doesn’t mean the property will be sold in a short time period; rather, the home will be sold short of what is owed on the loan. If a borrower cannot catch up on their mortgage payments, they must initiate the process of a short sale before a foreclosure comes into play.

How Does A Short Sale Work?

In order for a short sale in real estate to work, the property’s value must be less than what the homeowner/borrower still owes on the mortgage. The lender usually pardons the leftover balance of the loan. It doesn’t seem like the most ideal situation since the lender usually forgives the difference owed, but it’s still often preferred over a foreclosure.

Sometimes the lender uses a deficiency judgment that requires the borrower to pay the difference of the loan.

The Difference Between A Short Sale And A Foreclosure

If the homeowner never catches up on their mortgage payments and doesn’t pursue listing their home as a short sale, the lender (or bank) will start the foreclosure process. The lender does this by gaining ownership of the property (repossess), then selling the home to recoup the loan amount. Despite accepting a loss, the lender typically agrees with a short sale over a foreclosure.

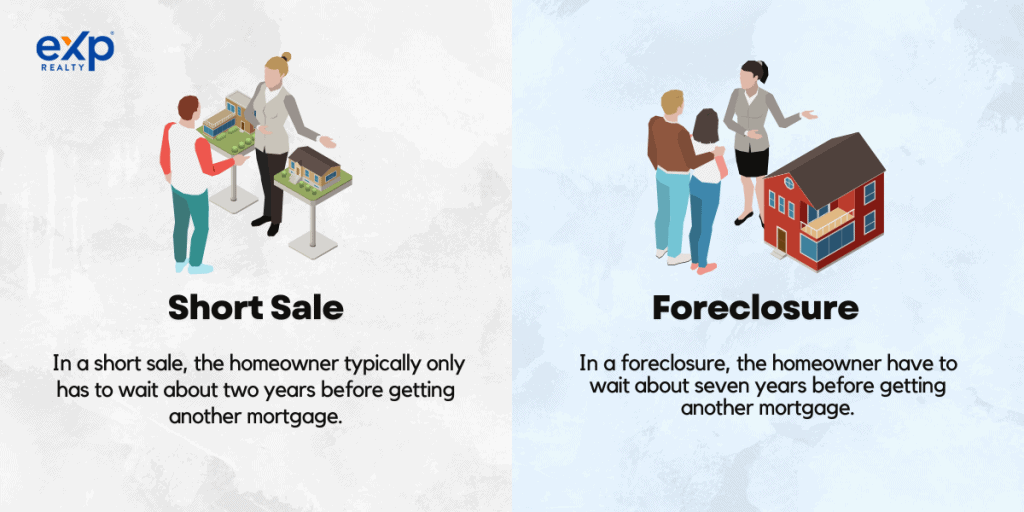

Homeowners choose to go the short sale route for a couple of reasons. One reason is that it’s their choice instead of them being forced into foreclosure. The biggest reason a homeowner chooses a short sale over a foreclosure, though, is that, in a foreclosure, they’d have to wait about seven years before getting another mortgage, whereas a short sale in real estate typically only has them wait about two years.

Lenders are usually willing to go the short sale route because they can get most of their money back without the hassle and cost of the legal process of foreclosure.

If the property couldn’t sell as a short sale, it would be foreclosed.

The Benefits Of A Short Sale

All parties involved can reap the benefits of a short sale transaction. It not only dampens the financial blow or burden from both the sellers and the lender, but it’s also an investment opportunity for the buyers.

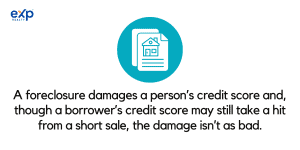

The benefits of a homeowner going through a financial crisis outweigh the consequences of a foreclosure process. For instance, a foreclosure damages a person’s credit score and, though a borrower’s credit score may still take a hit from a short sale, the damage isn’t as bad. It’s also common for the lender to write off the leftover debt as a loss. So, even though a homeowner may not make a profit from the sale, they’re not burdened with owing money on a property they do not own anymore.

The benefits of a homeowner going through a financial crisis outweigh the consequences of a foreclosure process. For instance, a foreclosure damages a person’s credit score and, though a borrower’s credit score may still take a hit from a short sale, the damage isn’t as bad. It’s also common for the lender to write off the leftover debt as a loss. So, even though a homeowner may not make a profit from the sale, they’re not burdened with owing money on a property they do not own anymore.

Another benefit to a homeowner choosing the short sale route is they don’t owe any fees like in a regular real estate transaction. The lender covers the fees commonly paid by the seller of a property.

Buyers also see benefits of buying a short sale home as they usually get a deal on a property from a seller eager to sell.

What Is The Downside Of A Short Sale On A Home?

Though some of the benefits of a short sale in real estate are great, many things can negatively impact the transaction and deter buyers.

- One of the biggest factors that makes a short sale transaction so different from other real estate transactions is how long they take. Buyers must practice patience since most short sale cases often last three to six months. This can also produce more paperwork for the buyer if they’re taking out a loan to purchase the property since their lender will likely need the most current pay stubs and bank statements at all times.

- Short sale properties are sold as-is and don’t typically come with a disclosure. It’s up to the buyer to perform all due diligence with inspections, making sure they know what they’re buying and they’re okay with not having the sellers make any repairs.

- Though it’s not as bad as a foreclosure, short sales damage the seller’s credit score. A seller will also have to wait to get another mortgage loan. (about two years).

- The lender holds negotiating power, which means the seller does not have a say in what their home sells for. The seller also cannot keep any of the profit since they owe it all to the lender.

- Occasionally, the lender will sue the seller to gain the rest of the money owed after a short sale. This is called a deficiency judgment.

Frequently Asked Question About Short Sales

What is the point of a short sale?

A homeowner who has fallen on hard financial times may seek a short sale transaction of their home in an attempt to wipe away mortgage debt and soften the blow to their credit score. It’s often the last resort before a property goes into foreclosure.

Can you offer less on a short sale?

Yes, buyers can offer less on a short sale, but the lender may not take much less than the list price since they’re selling the property short of what is owed and likely taking a loss.

Is a short sale a good idea?

A short sale in real estate is encouraged for sellers who cannot pay their mortgage as they’re able to recoup some of the money owed to the lender. It doesn’t damage their credit as bad as a foreclosure, and they don’t have to wait as long before buying another property. Buyers willing to accept the property as-is and don’t mind waiting typically see short sales as a good idea because of the investment opportunity.

What kind of market do short sales occur in?

Though short sales can happen in any market, you’ll likely see more short sales in a buyers’ market. Especially in a recession like back in 2007 to 2011 where there were several foreclosures too. The reason is, the lender needs to see what the home is worth at market value and if they can recoup their investment by selling at full price. Oftentimes they cannot, which makes them more agreeable to a short sale.

Selling or Purchasing a Short Sale in Real Estate

We hope this information has been helpful in learning what a short sale in real estate is. Whether you’re thinking of selling your home as a short sale or looking to buy a short sale property it’s always a good idea to get connected with a real estate agent who knows how to handle these transactions. If you haven’t found an agent yet, here is an article about questions to ask before hiring a real estate agent.